The Hidden Costs of Homeownership Every Buyer Should Budget For

For many people, buying a home represents stability, freedom, and the opportunity to build long-term wealth. After months of saving, getting pre-approved, touring homes, and finally receiving the keys, it's easy to feel like the biggest financial hurdle is behind you.

Then reality sets in.

The first utility bill arrives.

The HVAC system needs servicing.

The water heater suddenly stops working.

The landscaping needs attention.

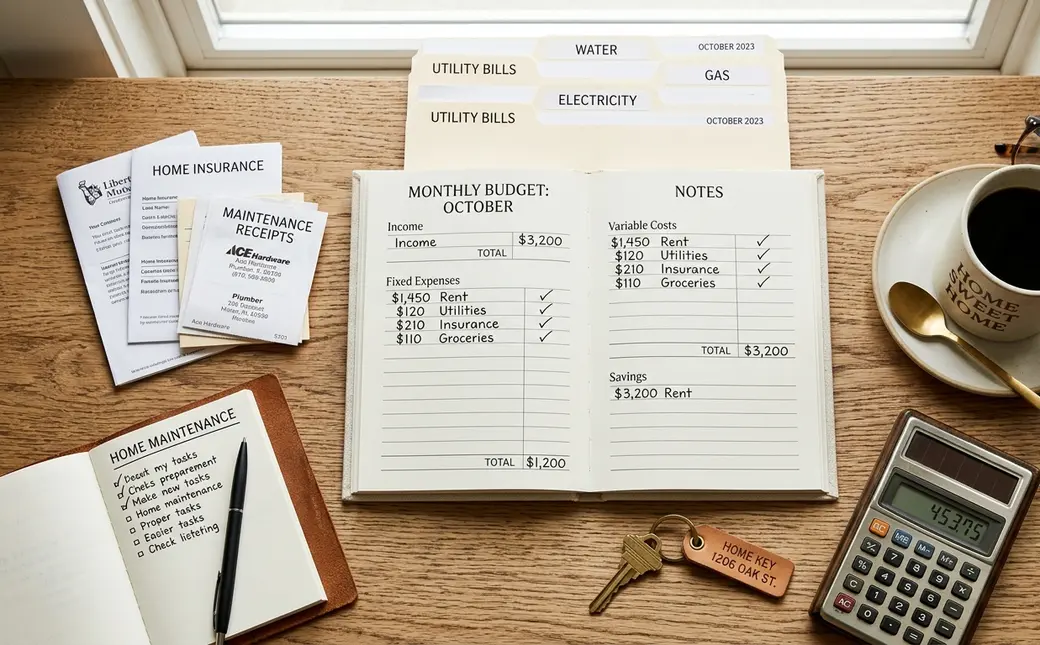

Owning a home comes with many financial responsibilities that renters often don't have to think about. While your monthly mortgage payment is likely your largest housing expense, it isn't the only one.

Understanding these additional costs before you buy can help you create a realistic budget, reduce financial stress, and enjoy homeownership with greater confidence.

Let's take a closer look at the expenses that many first-time buyers don't fully anticipate.

Your Mortgage Payment Is Only Part of the Monthly Cost

When buyers calculate what they can afford, they often focus on the principal and interest portion of their mortgage.

However, your monthly housing payment may also include:

- Property taxes

- Homeowners insurance

- Private Mortgage Insurance (PMI), if applicable

- HOA dues, if your community has a homeowners association

Together, these expenses can significantly increase your monthly housing costs.

That's why it's important to understand your estimated total payment—not just your loan amount.

Utility Bills May Be Higher Than You Expect

Many first-time homeowners are surprised by the cost of utilities, especially if they're moving from an apartment or smaller rental.

Depending on the size and age of your home, monthly utility costs may include:

- Electricity

- Natural gas

- Water

- Sewer

- Trash and recycling

- Internet

- Cable or streaming services

In Albuquerque, utility costs can also fluctuate throughout the year. Hot summers often lead to increased cooling expenses, while colder winter nights can increase heating costs.

When touring homes, ask about average utility costs whenever possible. It can provide a more accurate picture of your monthly budget.

Routine Maintenance Is Part of Homeownership

Every home requires regular maintenance.

Even newer homes benefit from ongoing care that helps protect your investment and prevent more expensive repairs later.

Typical maintenance includes:

- HVAC servicing

- Roof inspections

- Gutter cleaning

- Changing air filters

- Smoke detector batteries

- Pest control

- Caulking around windows and doors

- Landscaping and irrigation maintenance

These tasks may seem small individually, but together they become an important part of your annual homeownership budget.

Unexpected Repairs Will Happen

No matter how well a home has been maintained, unexpected repairs are part of owning property.

Common examples include:

- Water heater replacement

- Roof repairs

- Appliance breakdowns

- Plumbing leaks

- Electrical issues

- Garage door repairs

- HVAC repairs

These expenses rarely happen on a convenient schedule.

That's why many financial experts recommend keeping a dedicated home emergency fund.

Having savings available can turn an unexpected repair into an inconvenience instead of a financial crisis.

Don't Forget Lawn and Landscape Care

A beautiful yard adds curb appeal and creates enjoyable outdoor living space, but it also requires ongoing care.

Depending on your property, expenses may include:

- Lawn maintenance

- Tree trimming

- Irrigation repairs

- Gravel replacement

- Seasonal planting

- Weed control

- Outdoor lighting maintenance

In Albuquerque's high-desert climate, many homeowners choose low-water landscaping, but even xeriscaped yards require occasional maintenance.

Homeowners Insurance Doesn't Cover Everything

Homeowners insurance is essential, but it's important to understand what your policy does—and doesn't—cover.

Coverage varies by policy, and certain situations may require additional protection.

For example, some homeowners choose supplemental coverage for:

- Valuable personal belongings

- Flood-related risks (where applicable)

- Sewer backup protection

- Earthquake coverage in certain regions

Reviewing your policy annually with your insurance provider can help ensure your coverage still meets your needs.

Furnishing a Home Can Add Up Quickly

Many buyers focus entirely on the purchase itself without thinking about what happens after moving in.

Larger homes often require:

- Additional furniture

- Window coverings

- Patio furniture

- Storage solutions

- Area rugs

- Shelving

- Home décor

There's no need to furnish everything immediately.

Taking your time can help you stay within budget and make thoughtful design choices.

Moving Expenses Are Easy to Overlook

The cost of moving can vary significantly depending on your situation.

Possible expenses include:

- Professional movers

- Truck rental

- Packing supplies

- Temporary storage

- Cleaning services

- Utility connection fees

Planning for these costs ahead of time helps avoid surprises during an already busy transition.

HOA Fees Can Affect Your Monthly Budget

If you're purchasing a home in a community with a homeowners association (HOA), you'll likely pay monthly, quarterly, or annual dues.

HOA fees may cover services such as:

- Community landscaping

- Swimming pools

- Parks

- Clubhouses

- Private roads

- Exterior maintenance in some communities

Before purchasing, review both the cost of the HOA dues and the amenities or services they provide.

Property Taxes Can Change Over Time

Property taxes are an ongoing expense that should be part of your long-term financial planning.

Tax amounts can change due to:

- Property reassessments

- Local tax rates

- Home improvements

- Changes in exemptions

Understanding how property taxes work can help you budget more accurately over the life of your homeownership.

Energy Efficiency Impacts Long-Term Costs

Not all homes cost the same to operate.

Features that may reduce monthly utility expenses include:

- Newer windows

- Updated insulation

- High-efficiency HVAC systems

- Energy-efficient appliances

- LED lighting

- Smart thermostats

While energy-efficient homes may have a higher purchase price, they can help reduce ongoing operating costs.

Budget for Home Improvements

Even if your home is move-in ready, you'll likely want to make it your own.

Common improvements include:

- Interior painting

- Flooring updates

- Landscaping projects

- Kitchen upgrades

- Bathroom renovations

- New lighting fixtures

Rather than financing every project immediately, consider creating a long-term improvement plan that fits comfortably within your budget.

Build a Home Emergency Fund

One of the smartest financial habits a homeowner can develop is maintaining a dedicated emergency savings account.

Instead of waiting for something to break, prepare in advance.

Many homeowners set aside a small amount each month specifically for:

- Repairs

- Maintenance

- Appliance replacement

- Unexpected home expenses

This proactive approach makes homeownership much less stressful.

How Buyers Can Budget More Effectively

Before purchasing a home, consider creating a complete monthly housing budget that includes:

- Mortgage payment

- Property taxes

- Homeowners insurance

- Utilities

- HOA dues

- Maintenance savings

- Emergency repair savings

- Lawn care

- Home improvement fund

Looking at the full financial picture helps you choose a home that's comfortable not only to buy but also to own.

Work With Professionals Who Help You Plan Ahead

Buying a home involves much more than choosing a property.

A knowledgeable local Realtor can help you understand the full cost of homeownership, while your lender can explain your monthly payment and financing options.

Together, they can help you prepare for both the expected and unexpected expenses that come with owning a home.

Final Thoughts

Owning a home is one of the most rewarding investments many people will ever make.

It provides stability, the opportunity to build equity, and a place to create lasting memories.

But successful homeownership isn't just about qualifying for a mortgage.

It's about understanding the complete financial picture.

When you budget for maintenance, utilities, repairs, insurance, and other ongoing expenses, you're far more likely to enjoy your home without unnecessary financial surprises.

A well-planned budget allows you to focus less on unexpected costs and more on enjoying the home you've worked so hard to achieve.

Frequently Asked Questions

What hidden costs should I expect after buying a home?

In addition to your mortgage, budget for property taxes, homeowners insurance, utilities, maintenance, repairs, HOA dues (if applicable), landscaping, and home improvements.

How much should I save for home maintenance?

A common guideline is to set aside about 1% to 3% of your home's value each year for maintenance and repairs, though actual costs vary depending on the home's age and condition.

Are utility costs included in my mortgage payment?

No. Utilities such as electricity, water, natural gas, internet, and trash service are typically separate expenses.

Should I have an emergency fund as a homeowner?

Yes. Maintaining a dedicated emergency fund for unexpected repairs can help you avoid financial stress when major systems or appliances need attention.

Why is it important to understand the full cost of homeownership?

Knowing all of the ongoing expenses helps you create a realistic budget, choose a home you can comfortably afford, and enjoy homeownership with greater financial confidence.

Categories

Recent Posts

GET MORE INFORMATION