How to Create a Realistic Homebuying Budget in Albuquerque

One of the most important steps in the homebuying process happens before you ever tour a home, attend an open house, or make an offer.

It’s creating a realistic budget.

Many buyers begin their home search by asking:

"How much house can I afford?"

While that’s an important question, a better question might be:

"How much home can I comfortably afford while still maintaining my financial goals and lifestyle?"

A mortgage lender may approve you for a certain amount, but that doesn't necessarily mean you should spend that entire amount.

Creating a realistic homebuying budget helps ensure that homeownership remains enjoyable rather than financially stressful. It also helps buyers make confident decisions throughout the process and avoid common financial mistakes.

If you're planning to buy a home in Albuquerque, here’s how to build a budget that reflects the true cost of homeownership.

Start With Your Monthly Income

The first step is understanding your overall financial picture.

Calculate your:

- Monthly take-home income

- Additional income sources

- Consistent household earnings

Focus on income that is stable and predictable.

While bonuses, commissions, or occasional side income may help, your budget should primarily be based on income you can reasonably count on every month.

Understanding your income provides the foundation for every budgeting decision moving forward.

Review Your Current Monthly Expenses

Before determining what you can spend on housing, take an honest look at where your money currently goes.

Review expenses such as:

- Car payments

- Student loans

- Credit cards

- Insurance

- Childcare

- Groceries

- Subscriptions

- Entertainment

- Savings contributions

Many buyers are surprised by how much their current spending habits influence their homebuying budget.

A realistic budget should account for both housing expenses and the lifestyle you want to maintain after purchasing a home.

Understand the Difference Between Qualification and Affordability

One of the biggest mistakes buyers make is assuming that lender approval equals affordability.

Lenders evaluate:

- Income

- Debt

- Credit history

- Debt-to-income ratios

However, they do not always consider:

- Personal spending habits

- Travel goals

- Retirement savings

- Family plans

- Lifestyle preferences

Just because a lender approves a higher amount doesn't mean borrowing the maximum is the best decision.

Many homeowners prefer maintaining financial flexibility rather than stretching their budget to the limit.

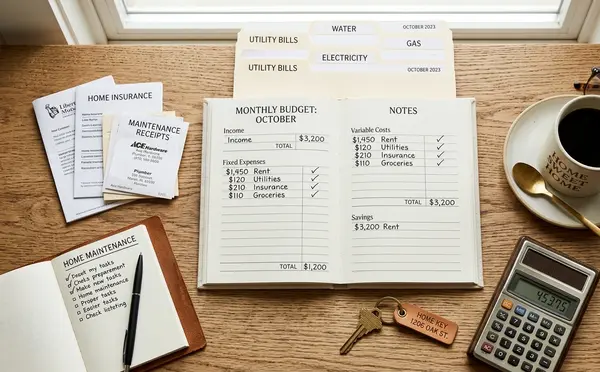

Estimate Your Monthly Mortgage Payment

Your mortgage payment is typically the largest part of your housing budget.

This payment usually includes:

Principal

The amount applied toward paying down the loan balance.

Interest

The cost of borrowing money from the lender.

Property Taxes

Taxes assessed by local governments.

Homeowners Insurance

Coverage that protects the property and homeowner.

Together, these costs often make up your monthly housing payment.

When budgeting, it's important to evaluate the total payment rather than focusing solely on the loan amount.

Account for Property Taxes

Property taxes are an ongoing homeownership expense that buyers should understand before purchasing.

Property tax amounts vary depending on:

- Property value

- Location

- Tax assessments

- Local regulations

Even though Albuquerque property taxes may be lower than some larger metropolitan areas, they still play an important role in your monthly budget.

Your lender can provide estimates based on the properties you're considering.

Include Homeowners Insurance

Homeowners insurance is required by most lenders and helps protect your investment.

Insurance costs vary based on:

- Home value

- Property characteristics

- Coverage levels

- Deductibles

Insurance should always be included when calculating total monthly housing expenses.

Budget for Maintenance and Repairs

One of the biggest differences between renting and owning is maintenance responsibility.

When something breaks in a rental property, the landlord typically handles the repair.

When you own a home, those costs become your responsibility.

Examples include:

- HVAC repairs

- Roof maintenance

- Plumbing issues

- Appliance replacement

- Landscaping upkeep

In Albuquerque, homeowners should also budget for:

- Roof maintenance due to sun exposure

- HVAC servicing during hot summers

- Irrigation system maintenance

- Exterior stucco upkeep

Many financial experts recommend setting aside funds each month specifically for maintenance and future repairs.

Don't Forget Utility Costs

Utility expenses can vary significantly depending on:

- Home size

- Age of the property

- Energy efficiency

- Occupancy levels

Utilities may include:

- Electricity

- Natural gas

- Water

- Sewer

- Trash services

- Internet

In Albuquerque, summer cooling costs can become a major consideration, particularly for larger homes or older properties with less energy-efficient systems.

Plan for Closing Costs

Many buyers focus heavily on saving for a down payment while overlooking closing costs.

Closing costs may include:

- Loan fees

- Appraisal fees

- Title fees

- Escrow fees

- Recording fees

- Prepaid taxes and insurance

These costs are typically due at closing and can add up quickly.

Understanding them early helps prevent financial surprises later.

Build an Emergency Fund

Homeownership comes with unexpected expenses.

For example:

- A water heater may fail.

- An HVAC system may need repairs.

- A roof issue may appear after a storm.

Having an emergency fund can help homeowners handle these situations without relying on high-interest debt.

Ideally, buyers should avoid using every available dollar for the down payment and closing costs.

Maintaining a financial cushion provides peace of mind after move-in.

Consider HOA Fees

Some Albuquerque communities have homeowners associations (HOAs).

HOA fees may cover:

- Community maintenance

- Common areas

- Recreational facilities

- Neighborhood amenities

These fees vary by neighborhood and should always be included when evaluating affordability.

A home that seems affordable initially may feel very different once HOA costs are added.

Think About Future Life Changes

Your budget should reflect not only your current situation but also your future plans.

Consider questions such as:

- Do you plan to grow your family?

- Are career changes possible?

- Do you anticipate major purchases?

- Will childcare expenses increase?

- Are retirement contributions a priority?

A realistic homebuying budget leaves room for life's changes and unexpected opportunities.

Avoid Shopping at the Top of Your Budget

Many buyers discover homes at the very top of their price range and become emotionally attached.

However, staying below your maximum budget often creates advantages such as:

- Lower monthly payments

- Greater financial flexibility

- Increased savings opportunities

- Reduced stress

Buying a home should improve your quality of life—not create financial pressure.

Work With a Local Albuquerque Real Estate Expert

A local Albuquerque real estate expert can help buyers understand:

- Neighborhood price trends

- Property taxes

- Utility considerations

- Market conditions

- Long-term value

Local guidance can help buyers identify homes that fit both their lifestyle goals and financial comfort zone.

Sample Albuquerque Homebuying Budget Categories

When creating your budget, consider including:

| Expense Category | Monthly Estimate |

|---|---|

| Mortgage Payment | Varies |

| Property Taxes | Varies |

| Homeowners Insurance | Varies |

| Utilities | Varies |

| HOA Fees | If applicable |

| Maintenance Savings | Ongoing |

| Emergency Fund Contribution | Ongoing |

Every buyer's situation is unique, but organizing expenses this way helps create a more complete financial picture.

Real-Life Example

Buyer A

Focuses only on the mortgage payment.

After moving in:

- Utility bills are higher than expected

- HVAC repairs arise

- Savings are depleted

Result:

Homeownership feels financially stressful.

Buyer B

Creates a complete budget that includes:

- Housing expenses

- Maintenance savings

- Closing costs

- Emergency reserves

Result:

Greater confidence, financial stability, and a more enjoyable homeownership experience.

Final Thoughts

Creating a realistic homebuying budget is one of the smartest things you can do before purchasing a home in Albuquerque.

A successful budget goes beyond the mortgage payment and considers:

- Property taxes

- Insurance

- Utilities

- Maintenance

- Closing costs

- Emergency savings

- Future financial goals

The goal isn't simply to buy the most expensive home you can qualify for.

The goal is to purchase a home that supports your lifestyle, protects your financial well-being, and allows you to enjoy homeownership for years to come.

With thoughtful planning and realistic expectations, you can enter Albuquerque's housing market with confidence and make decisions that support both your present and future goals.

FAQs

How much should I save before buying a home in Albuquerque?

In addition to your down payment, you should plan for closing costs, moving expenses, emergency savings, and future maintenance needs.

Should I spend the maximum amount a lender approves?

Not necessarily. Many buyers choose to stay below their approval limit to maintain financial flexibility and reduce stress.

What homeownership expenses are often overlooked?

Commonly overlooked expenses include maintenance, repairs, utilities, HOA fees, and emergency home repairs.

Are utility costs important when budgeting?

Yes. Utility costs can vary significantly depending on the home's size, age, and energy efficiency.

Why is an emergency fund important for homeowners?

Unexpected repairs can happen at any time. An emergency fund helps cover these expenses without creating financial hardship.

Categories

Recent Posts

GET MORE INFORMATION